Disclaimer: This is an article written in 2025 and some information may be outdated as the original medium article written was in 1H 2025 but there will be future series to reflect upon the developments of tokenized equity since the time of writing.

Introduction

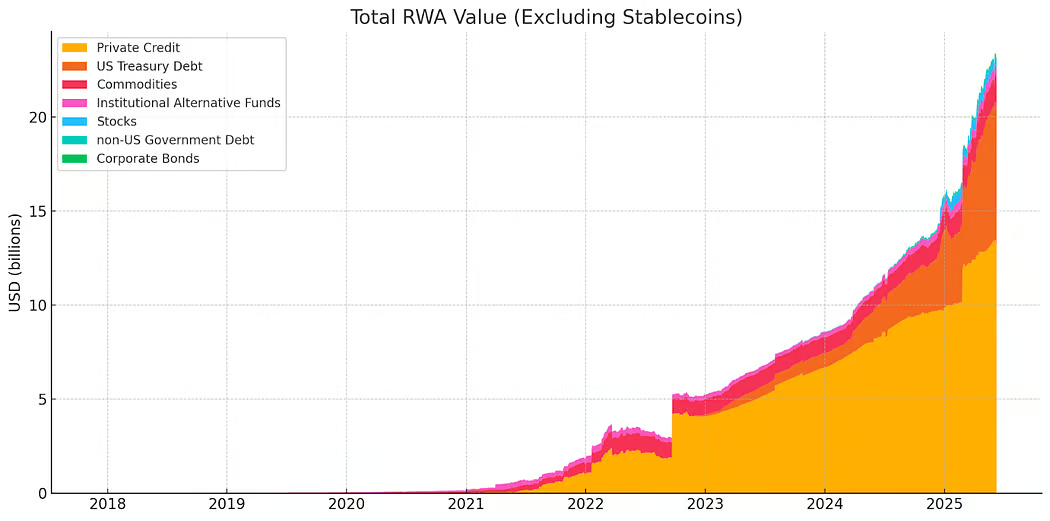

Institutional uptake of stablecoins and tokenized real-world assets (RWAs) has accelerated markedly: stablecoins now exceed $308 billion in market value, while RWA assets under management have risen from $20.6 billion to $23.23 billion year-to-date, propelled chiefly by tokenized private credit and Treasury products.

The successful issuance, settlement, and custody of these digital instruments have bolstered confidence in revamping legacy market rails to capture similar efficiency gains across additional asset classes — most notably equities, which stand out as the next logical frontier for institutional tokenization.

While nascent compared to stablecoins and tokenized treasuries, early players have made headways to make tokenized equity a long-term reality. Early pioneer, Backed Finance, began wrapping blue-chip stocks and ETFs into ERC-20 tokens and, in 2024, joined the Tokenized Asset Coalition before unveiling "xStocks," a new line of more than 55 equities and ETFs, got acquired by Kraken and announced major integrations across centralized and decentralized venues, marking a decisive step to bring tokenized equity mainstream.

Solana Foundation, AIX, Jupiter and Intebix also signed an MoU to develop a dual listing mechanism for companies seeking IPOs. Ondo Finance has also launched Ondo Global Markets, NYSE and Nasdaq both announced plans to roll out platform to facilitate tokenized securities trading. With major institutional backing, the fate of tokenized equity appears inevitable.

What Is Tokenized Equity And What Is Its Value Proposition?

The use of popular token standards enables tokenized equities to be used across different blockchain ecosystems (private or public) and unlock innovative DeFi use cases such as securities lending/financing, typically unavailable to retail users in traditional finance, enhancing capital efficiency as well.

Programmability of smart contracts used for collateral management can be applied to equity, unlocking greater liquidity just as cryptoassets are widely used as collateral in onchain financing. Already, Aave Horizon has demonstrated that RWA such as tokenized fund can be used as collateral.

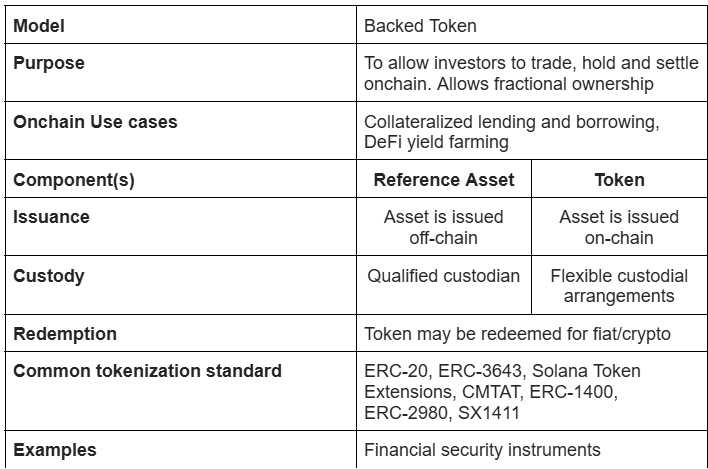

Tokenized equity requires a reference asset, which can either be a public or private stock, before a tokenized version can be created. The reference asset is stored in a regulated custodian for security, while holders of the tokenized shares can store them in their wallets.

A transfer agent is needed to play the role of managing transaction records and corporate actions. At present, most tokenized equity protocols do not permit redemption for the underlying shares; instead, redemption is executed for fiat or cryptocurrency.

The decision to issue tokenized shares hinges on leveraging the programmability and the efficiency of blockchain technology. Token programmability empowers issuers to embed regulatory requirements and other policies tied to the issued asset, automating complex processes.

A range of token standards — such as ERC-1400, ERC-3643, and Solana's token extensions — are already streamlining the onchain issuance process by offering institutional-grade features tailored to the specific requirements of issuers.

Effective stewardship of assets after tokenization is also critical, encompassing tax administration, ongoing regulatory review, periodic asset valuation, oracle risks, and the coordination of corporate actions.

Current State of Tokenized Equity

Currently, tokenized equity remains in a nascent stage with a combined market capitalization of $913M, paling in comparison to the size of traditional equity capital market but more than 2.5x the performance statistics shown below. Most of the tokenized equity now come from Ondo Global Markets, which is more than double the size of xStocks. Ethereum remains the preferred chain for tokenized equity, followed by Solana and Algorand.

Regulations

In terms of regulations, supportive regulatory policies have facilitated initial adoption of tokenized equities:

- Switzerland — Switzerland DLT Act: Under this Act, companies are allowed to issue their shares digitally on a blockchain, which has enabled numerous Swiss companies to tokenize their shares to access liquidity while being regulatory compliant.

- USA — U.S Securities Act Reg. S Exemption: Regulation S is a safe harbor under the U.S. Securities Act of 1933 that allows offerings and sales of securities to proceed without SEC registration, provided no directed selling efforts are made in the U.S. and no U.S. persons participate during the distribution period.

- Germany — Liechtenstein Blockchain Act: Enacted in October 2019 and effective January 2020, the Token and Trusted Technology Service Provider Act (TVTG) establishes a comprehensive legal framework for tokenized rights and assets — including equity, debt, and more — by introducing the Token-Container Model, where any right can be embedded into a token. It mandates regulatory oversight and participant licensing under the Financial Market Authority of Liechtenstein.

Key Players

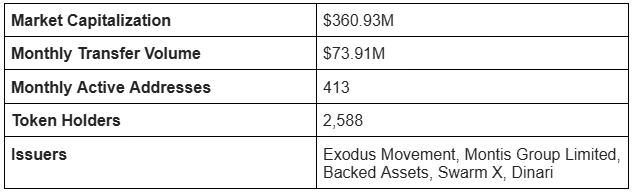

Backed Finance

Backed Finance began wrapping blue-chip stocks and ETFs into ERC-20 tokens. In 2024, they joined the Tokenized Asset Coalition before unveiling "xStocks," a new line of more than 55 equities and ETFs. They got acquired by Kraken and announced major integrations across centralized and decentralized venues.

Dinari

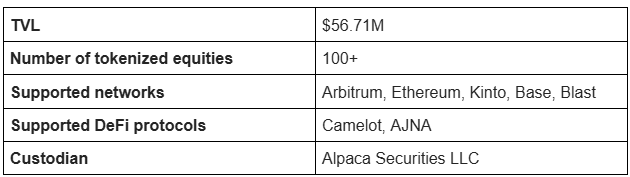

Dinari, Inc is a U.S. based registered transfer agent with the SEC that leverages dShares to enable equity tokenization. Each dShare represents an off-chain stock with a 1:1 backing for every dShares issued. To mint dShares onchain, businesses will first have to undergo KYB and customers to undergo KYC.

A custodian will handle the custody of the underlying reference asset purchased when a user purchases a dShare. dShare tokens are ERC-20 compatible and can work across Ethereum, Base, Blast and Arbitrum One and Kinto.

To cater to regulatory requirements, the protocol regularly reports dShares reserves and uses independent third party auditors to verify reserves. Tokens issued also have transfer restrictions applied based on the regulatory requirements of the reference asset domiciled. However, current dShares are not entitled to voting rights although they can benefit from dividend payouts of the underlying reference asset as well as fractional shares ownership.

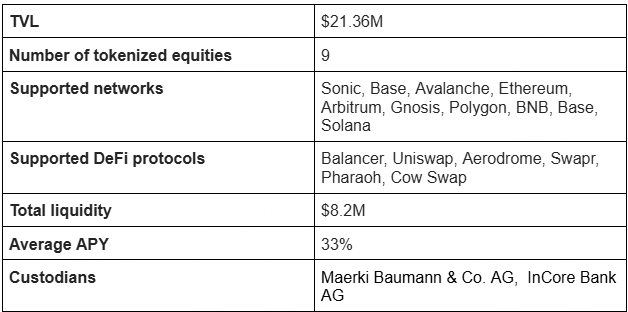

Swarm X

Swarm is a Germany-based tokenization platform regulated by the Federal Financial Supervisory Authority (BaFin). SwarmX GmbH, the issuing SPV, buys the target security and parks it with an institutional custodian.

Once a token-trustee verifies custody, an ISIN-linked security token is minted on Polygon and made tradable through Swarm's dOTC and AMM pool. Tokens are fully-backed, redeemable for underlying value (USDC) once aggregate requests hit $100K, and subject to monthly reserve disclosure.

Blockchain Infrastructure

Solana

Designed as a high-speed, low cost L1 network, Solana has ramped up its efforts to drive the adoption of tokenized equities on its network. Sol Strategies, a publicly listed company building the infrastructure for Solana, has signed an MoU with Superstate to explore the issuance of the company's common shares on the Solana blockchain through Superstate's 'Opening Bell' tokenization platform.

Additionally, Solana Foundation also signed an MoU with Astana International Exchange (AIX), Intebix, and Jupiter to explore the development of dual listing mechanism for companies listing through AIX. Solana's token extension offers greater token flexibility and enables compliance policies to be embedded within the token.

Ethereum

The pioneer in tokenized securities via ERC-20 and newer ERC-3643 standard (built for permissioned, compliant securities like tokenized equity). ERC-3643 meets stringent regulatory requirements by embedding investors' rules and offering rules, ensuring compliance at the smart contract level. Today, Ethereum stands as the largest network for RWA, commanding a 60% market share in tokenized RWA.

Plume Network

Plume Network recently launched its Mainnet (Plume Genesis), onboarding over $247 million in tokenized RWAs (including private equity and treasuries). Built with a dedicated institutional RWA tokenization framework and protocols (Arc & SkyLink) to support cross-chain issuance and compliance. The platform's ecosystem now includes more than 200 projects.

Wallet and Custodians

Trust Wallet

Trust Wallet, a non-custodial wallet with more than 15 million monthly active users, recently announced that it will start supporting RWA assets.

Taurus

Taurus, an enterprise digital asset custody and tokenization platform provides an end-to-end tokenization solution that is in compliance with Swiss Law for clients looking to tokenize any types of real world assets.

Fireblocks

Fireblocks is a digital asset infrastructure provider offering a comprehensive platform for enterprise digital assets needs. In terms of tokenization, Fireblocks also provides a comprehensive service ranging from token minting, management, distribution and custody.

Challenges

Limited trading hours in traditional equity markets could impede the issuer's ability to trade the shares after market hours to maintain fully-backed collateral value. During the occurrence of significant events post market hours, issuers may be unable to rebalance the collateral, leading to temporary mismatches in asset backing or heightened price volatility on secondary markets.

If tokenized equity does not confer the same benefits as traditional equity such as voting rights, dividend rights among others, this could dampen adoption as well, especially among institutional and activist investors seeking enforceable legal claims.

Privacy is an important consideration for financial institutions when executing transactions. However, the lack of a universal, industry-wide cryptographic standard for privacy has led to a slow uptake from institutional investors.

With a rising number of institutional-grade blockchains, the issue of liquidity fragmentation is becoming more apparent. Many of these tokenized equity are faced with poor liquidity in DEX pools.

Conclusion

As legacy market rails begin to plug directly into public-chain infrastructure and regulators formalize rule-sets for tokenised securities, the main frictions — settlement plumbing, compliance, and custody — are steadily being removed.

With clear guardrails around KYC, AML, and investor protection baked into smart-contract standards, banks and transfer agents are positioned to adopt tokenised shares for collateral management and 24/7 trading, with retail venues following as liquidity deepens.

Notably, BX Digital, a subsidiary of Boerse Stuttgart Group, has received the FINMA license for a DLT trading facility in Mid-March is working with 5 partners who will help to drive the settlement of tokenized assets such as shares, bonds and funds between institutional market participants.

Players like Chainlink are also spearheading adoption and liquidity to public chains via its Chainlink Runtime Environment (CRE) which helps to facilitate a secure, simultaneous, and seamless transaction experience between private permissioned chains and public permissionless chains.

In summary, while the tokenized equity market remains nascent today, it is far from a passing trend. Supported by institutional adoption, technological standardization, and regulatory clarity, tokenized equity is poised to scale gradually yet sustainably as traditional and decentralized systems converge.