Macro Overview

January was defined by four key themes: regulatory uncertainty as the CLARITY Act stalled in the Senate, heightened geopolitical concerns between US, Europe, and Greenland, capital outflows into AI adjacent equity names (particularly in US, China, and Hong Kong) and commodities outperformance as the traditional safe haven attracted flows amid risk-off sentiment. These factors have posed headwinds for the crypto market for a start as total cryptocurrency market capitalization contracted $180B throughout January amid prevailing risk-off sentiment as reflected by both the Fear and Greed Index which stood at 28 (fear zone) and altcoin season index at 31.

Bitcoin consolidated within the $82,000–$95,000 range struggling to reclaim its October 2025 all-time high of ~$126,000. Bitcoin ETFs experienced an outflow of $1.6B in January while Ethereum ETFs saw outflows of $342M and struggled below the $3,000 psychological level. The RWA sector emerged as a bright spot, with tokenized assets reaching $24.26B in TVL as institutions shift from pilot experiments to real world deployment of assets and systems that facilitate tokenized assets.

Bitcoin

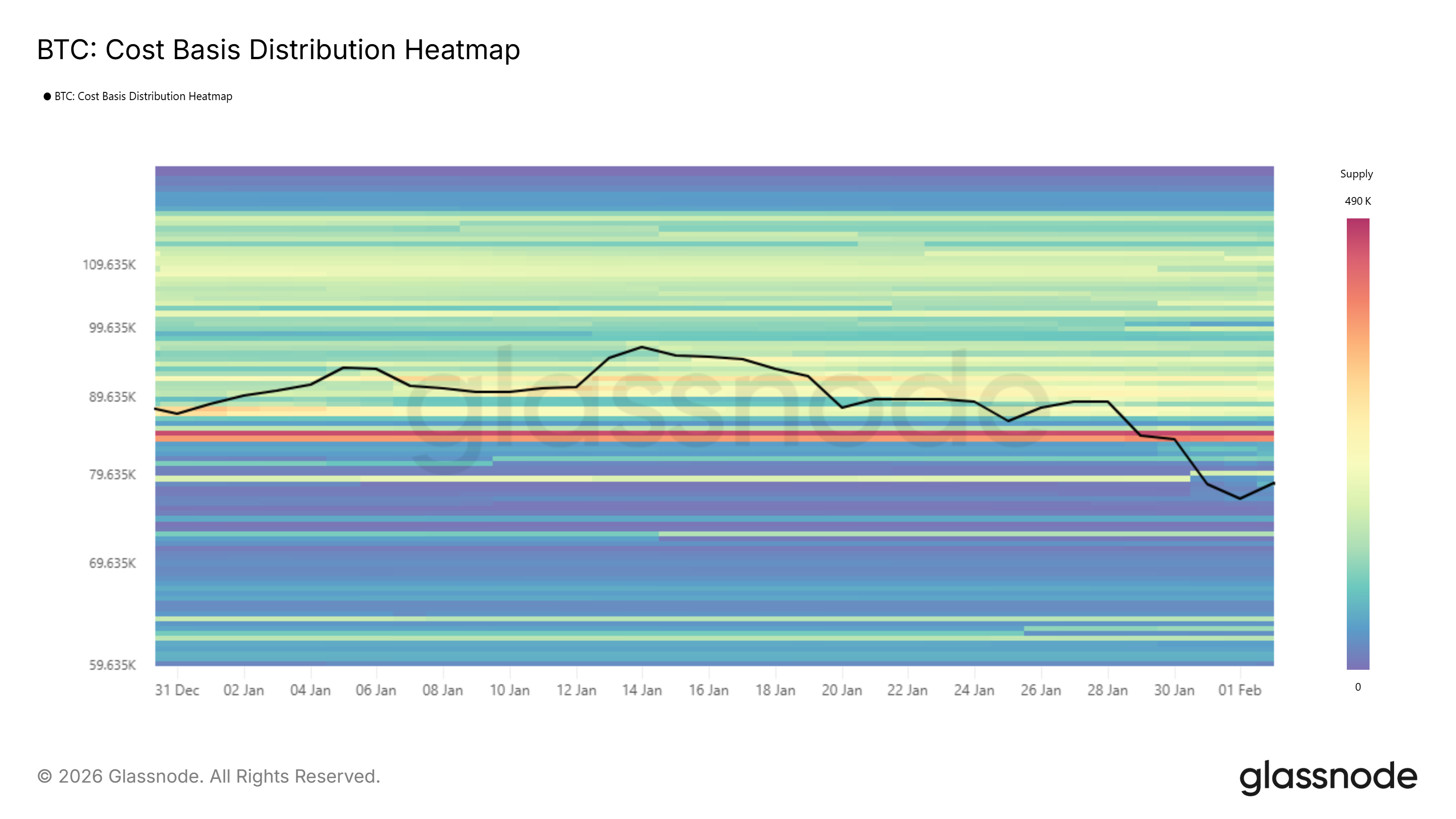

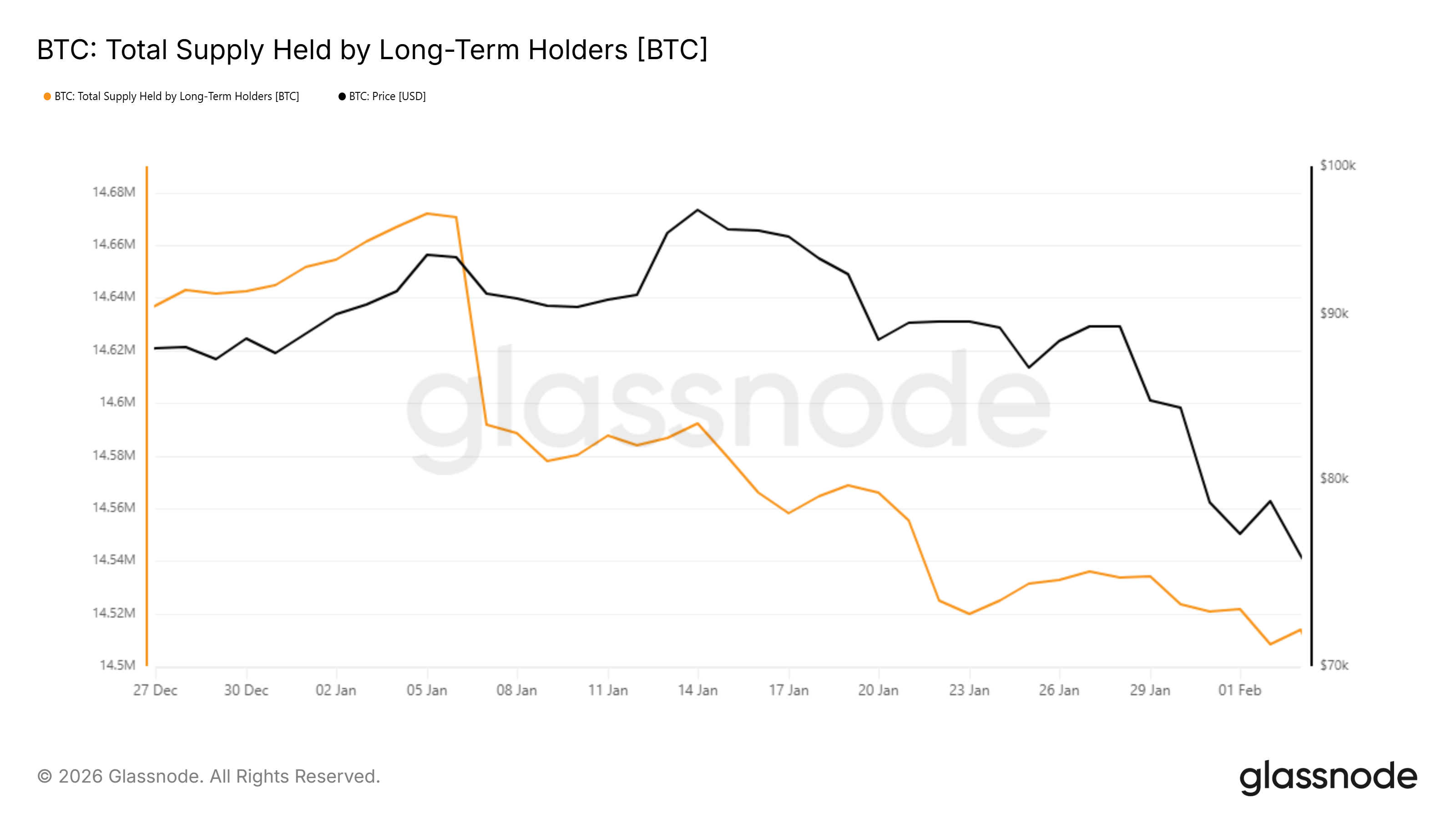

Bitcoin fell 6.9% MoM in January to $81,181, which represented a significant pullback from the $126,000 all-time high reached in October 2025, with the asset now trading ~35% below peak levels. Bitcoin's Sharpe ratio entered negative territory, underscoring the unprofitable macro setup for investors in the current market environment. The asset currently trades below both its 100-day MA (~$99,569) and 200-day MA (~$104,653), with key cost basis and resistance formed at $84K–$85K.

The current price setup remains an attractive entry for institutions such as Strategy which has added more than 40,000 BTC at an average price of $93,456. Strive has also made a full stock acquisition deal of Semler Scientific, consolidating its Bitcoin holdings to become the 11th largest publicly traded Bitcoin treasury while also taking over Semler Scientific's healthcare business. Bitcoin ETF flows presented a mixed picture for institutional Bitcoin appetite with more than $1.6B in outflows recorded in January. Bitcoin accumulation continues in selected firms, while other institutional and retail investors err on the side of caution as Bitcoin supply held by long term holders got offloaded.

Ethereum and L2s

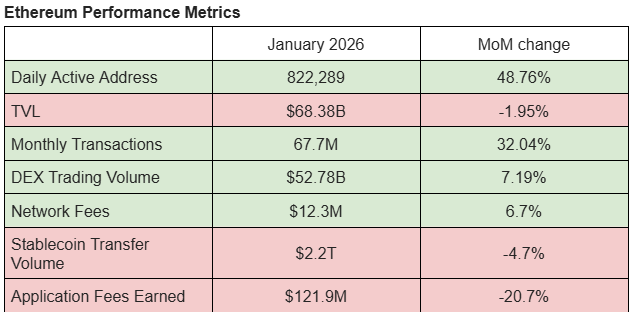

Ethereum's price faltered in January, falling ~19% MoM amid a challenging macro climate. The selloff persisted despite Bitmine Immersion acquiring more than 133,000 ETH during the month and staking close to 50% of its holdings. ETF outflows further subdued prices as more than $340M left the asset.

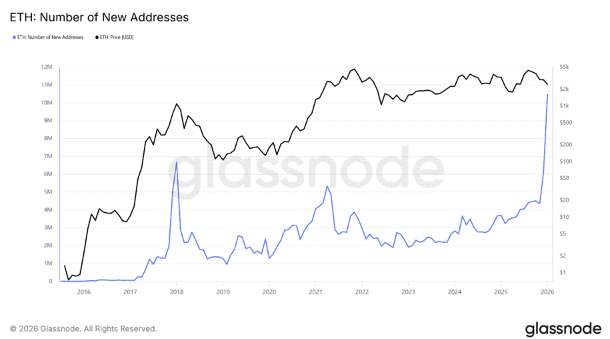

Notwithstanding price performance, network adoption has grown as both daily active addresses, DEX trading volume, and monthly transactions soared in January against the backdrop of significantly lower network fees post Fusaka Upgrade. The number of monthly new addresses hit an all-time high of 10M in January, underscoring the increasingly fundamental role of Ethereum for DeFi, stablecoin, and RWA activities. However, this has also made the cost of address poisoning attacks relatively cheap since the cost of sending malicious transactions became significantly lower after the Fusaka Upgrade. Security researcher Andrey Sergeenkov cautioned that part of the increased network activity came from large scale spam campaigns. While TVL declined in USD terms, TVL in ETH grew driven by increased institutional staking activities.

Moving forward, the Glamsterdam upgrade targeting 1H 2026 will introduce parallel processing capabilities and raise the gas limit from 60 million to 200 million, significantly expanding throughput. The Hegota upgrade planned for 2H 2026 will implement Verkle Trees for improved state management. We expect to see Ethereum close the gap with L2s as costs and scalability bottlenecks are being addressed through further upgrades.

Other notable developments:

- EF formed a new Post Quantum team and hired Ben Edgington to work on fast finality for the network.

- Vitalik proposed introducing native DVT for ETH stakers.

- JP Morgan launched MONY, a tokenized money market fund on Ethereum.

- Fidelity is launching FIDD stablecoin on Ethereum.

- Ethereum Magicians published their L1 zkEVM roadmap for 2026.

- ERC-8004 is now live on Ethereum, enabling agents to be identified and tracked and validated onchain.

- Lido rolled out V3 protocol and stVaults on Ethereum.

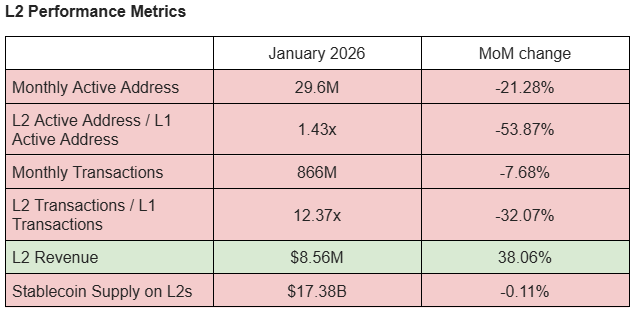

As the cost of transactions on Ethereum slides, the competitive advantage of L2s has weakened notably as usage shifted back to the L1. Meanwhile, L2s' revenue capture improved in January, led by Base which more than doubled its revenue in January. This can be attributed to increase in DEX trading volume and lending activity. DEX trading volume on Base increased from ~$450M in early January to a peak of ~$3.5B on 19 January, surpassing that of Ethereum and BNB for the first time. Both Aerodrome and Uniswap saw growth in trading volumes while PancakeSwap volume declined.

TVL on Base increased as demand for curated yield vaults accelerated, led by Steakhouse Financial and Gauntlet. Steakhouse Financial's TVL on Base rose from $550M to $840M, supported by its partnership with Coinbase and Morpho, which provides Coinbase users access to approximately 4.2% APY. Gauntlet's TVL on Base similarly expanded from ~$289M to $420M, driven by a series of partnerships, including its recent Earn integrations with SafePal and KAST.

Hyperliquid

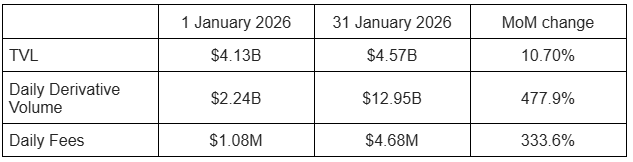

While the broader crypto market was embattled under the current uncertain macro landscape, Hyperliquid continued to benefit from market volatility in January as perp DEX volume increased by 22.7% MoM to reach $211.6B. The elevated trading volume coupled with more than $50M in token buybacks led HYPE to gain ~17% MoM defying the broader market downturn.

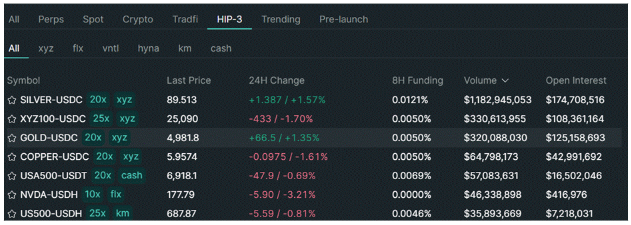

The protocol has evolved from a crypto-focused perpetual DEX in 2025 into a universal exchange following the launch of the HIP-3 upgrade. HIP-3 enables the permissionless deployment of new markets, offering broader asset coverage alongside a fee-sharing mechanism for market deployers. The framework introduces a 500,000 HYPE staking requirement, which helps mitigate sell pressure on the native token, filters out low-quality or spam deployments, and incentivizes serious participants to launch markets while leveraging Hyperliquid's network effects.

To date, the platform has emerged as a hub for commodities perpetual trading, with SILVER-USDC recording over $1B in 24-hour trading volume and approximately $175M in open interest at the time of writing, highlighting strong user demand for leveraged exposure beyond crypto assets. Increasingly, Hyperliquid is establishing itself as a decentralized platform for institutional liquidity, with 24h trading volume and open interest surpassing OKX and Bitget on several occasions.

Key Performance Metrics

Real World Assets (RWA)

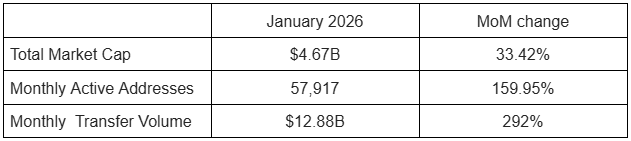

The RWA sector expanded in January, growing TVL by 16.85% MoM to $24.26B. Specifically, the tokenized commodities sector emerged as January's standout performer, with total TVL climbing more than 33% MoM from ~$3.5B to ~$5.3B. Active holders also more than doubled to 57,917 fueling monthly transfers volume to correspondingly surge more than 290%. Leading the growth is XAUT which saw a wave of exchange listings that enhanced token distribution, leading to a circulating supply of $2.57B, and capturing more than 50% of the tokenized commodities market.

This growth occurred against a backdrop of declining crypto prices, underscoring onchain interest in capitalizing on gold's price appreciation and increased adoption of tokenized commodities for portfolio diversification. However, the returns for tokenized commodities still lagged spot gold returns highlighting the trade offs between liquidity as well as 24/7 trading functionality. Moving forward, as greater volume moves onchain as part of users' portfolio diversification and trading efficiency, we expect this pricing discount to narrow.

Tokenized Commodities Performance Metrics

Tokenized securities, especially equities, could accelerate soon as January marked an inflection point for institutional adoption and regulatory approval. Figure unveiled their OPEN platform for tokenized equities enabling native stock issuance and trading directly on their provenance blockchain with shareholder rights being embedded into tokenized securities. Chainlink launched 24/5 onchain data streams for tokenized US equities and ETFs. Exchanges like Nasdaq and NYSE also announced plans to launch their own tokenized securities trading platform that confer tokenized equity the same shareholder rights as traditionally issued equity securities, although these plans are still subjected to regulatory approval.

If launched, these could be a double edge sword for existing players in the ecosystem. On one hand, we could see exponential growth in stablecoin adoption and blockchain revenues. On the flipside, smaller tokenized securities platforms could face greater competition due to a lack of large network effects while some platforms do not confer the same shareholder rights as traditional equities, putting them at a disadvantage should traditional incumbents scale.

Meanwhile, since Ondo Global Markets launched in September 2025, it has quickly overtaken Backed Finance xStocks in terms of TVL with Ondo Global Markets having 3.5x more TVL than Backed xStocks. Collectively, the size of tokenized equities has also crossed the $1B milestone.

Tokenized Equities Performance Metrics

Other notable developments:

- Maple Finance launched on Base.

- Ondo Global Market expands to Solana.

- LSE launched its 24/7 blockchain based settlement platform for tokenized bank deposits.

- Galaxy debuts $75M tokenized CLO on Avalanche.

- Ripple provided $150M financing to LMAX Group in exchange for RLUSD being used as a core asset on the LMAX Group platform for institutional clients.

- South Korea approved tokenized securities framework with legal effect expected in January 2027 after presidential approval.

Stablecoins

The stablecoin market declined in January from ~$307B to ~$305B, underscoring risk off appetite in crypto as well as capital being deployed to capitalize on other opportunities in AI/tech equities and commodities. While both USDT and USDC contracted, USDC experienced a sharper outflow of ~$6B leading to a marked decline in market share.

Despite market structure bill delay over contentions on stablecoin yields, yield-bearing stablecoins like Ondo's USDY climbed from $626M to $1.25B in January. $U by United Stables launched on 18 December 2025 on BNB and has benefited from early traction with circulating supply soaring to $759M in January tied to deep ecosystem integration with leading DeFi platforms and major exchange listings.

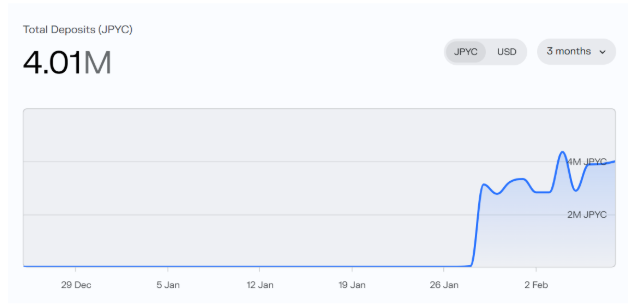

Beyond USD stablecoin, yen-pegged stablecoin JPYC made further headways onchain with integrations with major DEX protocols. Currently, most of the liquidity is seen on Uniswap V4 on Polygon and Ethereum. JPYC was also integrated on Morpho by risk curator Steakhouse Financial, with the stablecoin witnessing more than 3.3M JPYC being deposited on Morpho Polygon since its late debut in January.

Overall, stablecoin adoption continued to remain steady with monthly stablecoin transfer addresses reaching its highest level of 29.2M users over the past year with strong user growth seen in USD1, USDS and AUSD which witnessed 37%, 57%, 15% MoM growth in monthly stablecoin transfer addresses.

Other notable developments:

- USD.ai approved a $500M loan for an Australian AI startup.

- Circle gateway now live on Solana.

- Visa now captures ~90% of all stablecoin card transactions.

- BVNK and Visa partners to allow BVNK to power Visa Direct.

- South Korean firm KB Bank files for stablecoin credit card.

- USDe now listed on Upbit.

- USDG launched liquidity rewards for Aave lenders.

- Interactive brokers unlock 24/7 funding with USDC, with plans to roll out RLUSD, and PYUSD.

- JPYC, yen-pegged stablecoin, plans to reach $10T yen in circulating supply in the next 3 years.

- Trip.com tests stablecoin payments overseas, offering USDT, USDC for prepaid bookings.

Notable M&A / Fundraising

Fundraising and M&A activity rebounded from December lows with ~$939M closed deal value across 53 projects in January.