Macro Overview

February's crypto markets were defined by a severe macro-driven deleveraging event on February 5, when Bitcoin plummeted over 14% — one of the steepest single-day declines on record — triggering $2.1 billion in liquidations, the month's largest. Unlike crypto-native shocks, this crash stemmed from Trump's escalating tariff rhetoric and heightened U.S.-Iran geopolitical tensions, driving capital rotation from risk assets to safe havens as spot gold surged past $5,172/oz.

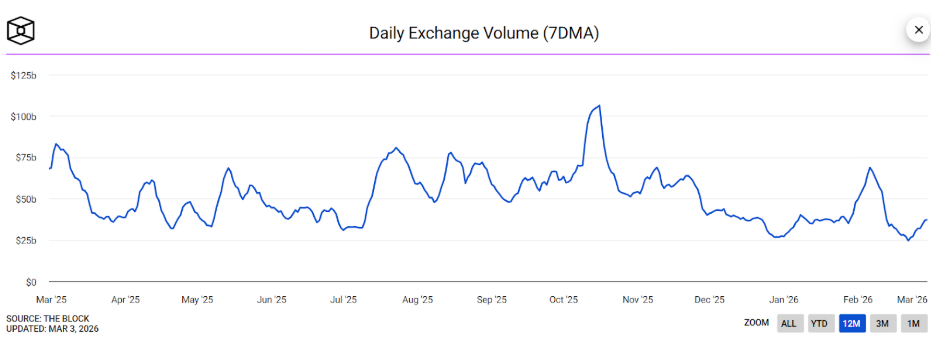

Structural fragility amplified these moves. Daily exchange volumes collapsed from $106 billion to $35 billion year-over-year, with thin liquidity exacerbating intraday volatility. Institutional sentiment deteriorated as Bitcoin ETF holders faced widespread losses, fueling $206 million in February outflows. However, select institutions — including Strategy, Mubadala Investment Company, Al Warda Investments, and Binance — capitalized on the dislocation, accumulating Bitcoin during peak fear.

Rounding up, three macro headwinds dominated the month: (1) Trump's tariff escalation threat and heightened US-Iran geopolitical tensions spurred broad risk aversion; (2) the nomination of monetary policy hawk Kevin Warsh as Fed Chair raised concerns over central bank independence and future directions of monetary policy, lifting the DXY and pressuring BTC; and (3) legislative impasse over the CLARITY Act's stablecoin yield provisions introduced near-term regulatory uncertainty.

Besides the US, regulatory progress continues to advance globally. In Hong Kong, the first licenses are expected to be issued to stablecoin issuers in March. UK's FCA has also enabled 4 firms to be part of the stablecoin regulatory sandbox to test stablecoin products in real world settings alongside appropriate safeguards. South Korea is also planning a new bill which could mandate crypto influencers to disclose their asset holdings and paid promotions.

Bitcoin

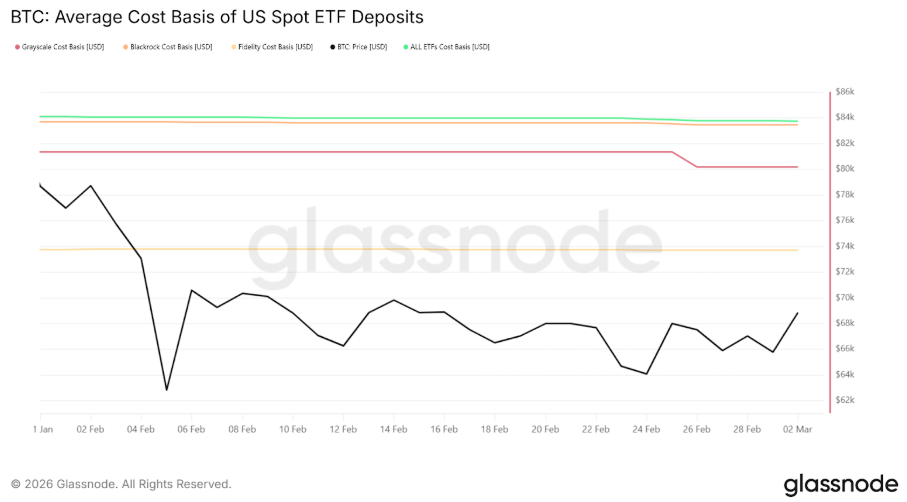

Opening the month at $78,626, BTC briefly found support above $73,000 before the February 5 crash pushed it below $63,000 intraday. The subsequent recovery to $70,000 proved a bear-market relief rally; Bitcoin struggled to sustain gains above that level, fading back to the $63,000–$68,000 range by month-end. With most BTC ETFs' cost basis being around $83.7K, institutional demand has noticeably weakened as returns become negative for the first time this year, driving outflows and redemptions that further limit upside.

On the mining side, more miners have now pivoted to the lucrative AI/HPC sector with Bitdeer being the latest to jump onto the bandwagon. The Bitcoin miner sold all of its Bitcoin treasury to support its transition to become an AI datacenter. Digital asset corporate treasuries other than Strategy have shown signs of cracks as mNAV widens. GD Culture, a Bitcoin treasury firm, recently approved the sale of its 7,500 BTC for share repurchase as its mNAV stood at around 0.5. Meanwhile, the largest digital asset treasury firm, Strategy, doubled down on its Bitcoin purchases to capitalize on price weaknesses, bringing its total holdings to 717,722 BTC with average acquisition cost of $76,019.

Ethereum & Layer 2s

Ethereum fell to a low near $1,800 in early February — its weakest level since May 2025 — as the broader market rout overwhelmed Ethereum-specific catalysts. By month-end, ETH had closed below $2,000, trading within a tight $1,850–$2,000 range that reflected investor indecision. The ETH/BTC ratio continued its multi-month compression as Bitcoin dominance held up better relatively speaking — a dynamic consistent with early bear-cycle behaviour where BTC dominance tends to expand as liquidity tightens.

Despite the price weakness, Ethereum's fundamental development pipeline was arguably its most active in years. The Ethereum Foundation unveiled "Strawmap" — a draft research roadmap to 2029 — targeting near-instant transaction finality (6–16 seconds vs. the current ~16 minutes), native privacy features, and post-quantum cryptographic upgrades. Vitalik Buterin separately published a detailed plan to protect Ethereum's cryptographic infrastructure against future quantum computing threats. The Glamsterdam upgrade, scheduled for H1 2026, remains on track to increase the gas limit to 100 million and beyond per block, expand blob parameters for L2 support, and implement enshrined proposer-builder separation (ePBS).

While DeFi TVL on Ethereum broadly declined in February, there were pockets of growth seen in RWA assets, savings and DeFi vault expansion, underscoring sentiments shifting towards commodities and yields with low correlation to crypto markets.

The Ethereum Foundation also began staking portions of its ETH holdings for the first time, signalling a strategic shift toward active participation in network security and yield generation. BitMine Immersion (BMNR) increased its ETH treasury by over 179,000 ETH during the month, a notable institutional accumulation move despite the price weakness.

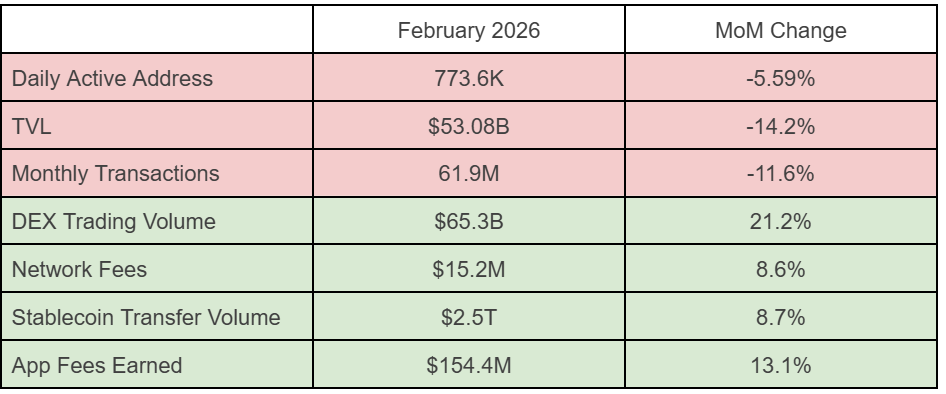

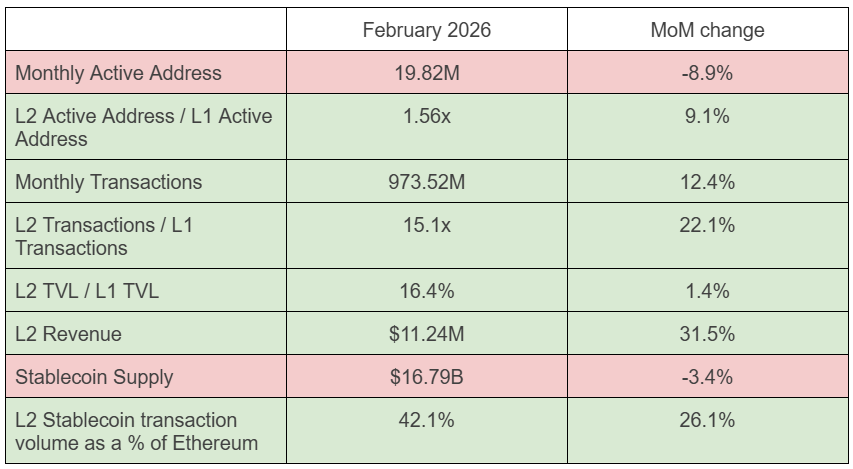

Performance Metrics of Ethereum

Ecosystem Expansion Metrics in February

L2 Performance Metrics

Overall, despite the broader risk-off sentiment, usage metrics on L2s remained resilient, underscoring the stickiness of L2 due to cost and speed advantages and its growing dominance in the payments landscape.

L2s that saw notable growth in February are MegaETH, Mantle, and Plume which expanded their TVL by 571%, 160%, 13.8% MoM respectively. Mantle growth can be attributed to the launch of Aave V3 alongside token incentives by Mantle and Aave which quickly attracted over $550M in 2 weeks since launch.

Other L1s — Provenance

TVL on Provenance blockchain, currently being operated by Figure Technologies, has significantly expanded their TVL in February, growing from ~$940M to $1.5B largely driven by an increase in tokenized HELOC loans.

Other L1s — Hyperliquid

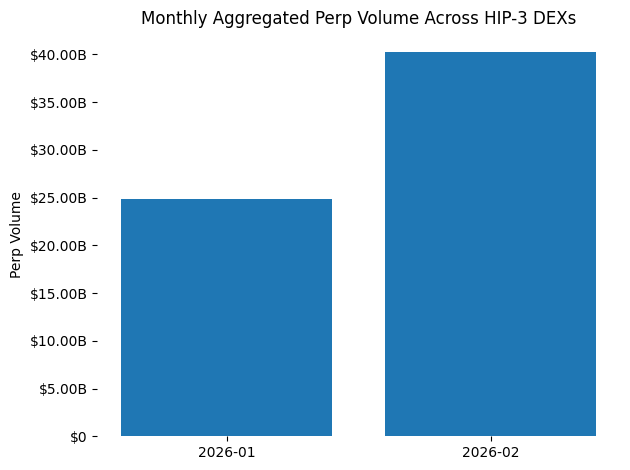

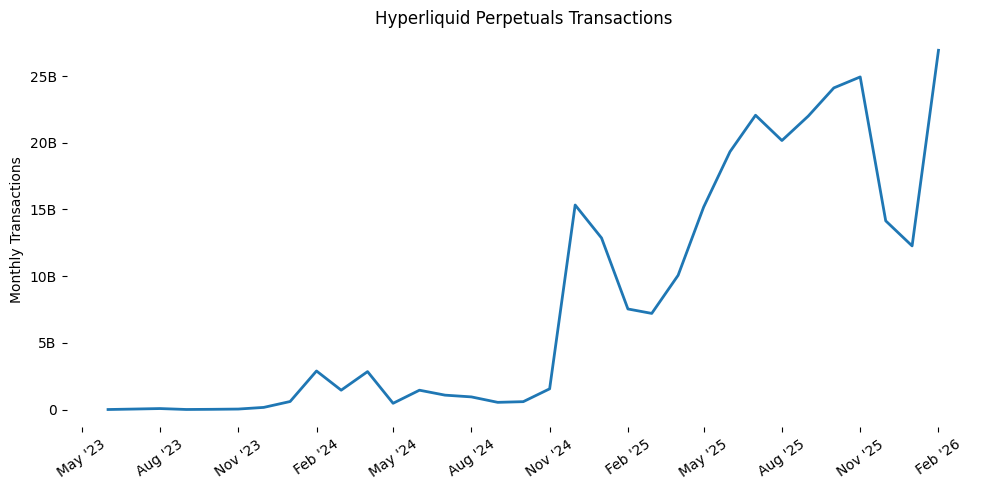

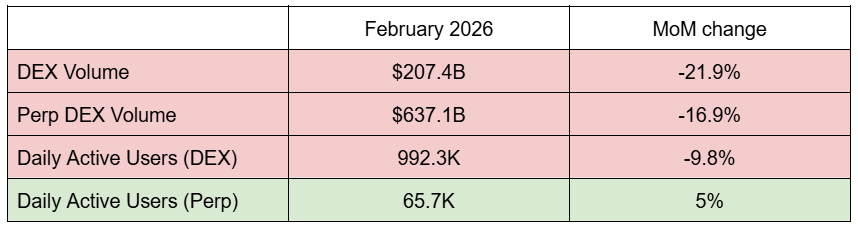

February marked Hyperliquid's first stress test event for TradFi-linked assets amid rising macroeconomic tensions. With margin requirements on CME rising from 6% to 8% for gold and 11% to 15% for silver after the flash crash event on 30 January, this has driven flocks of users to Hyperliquid, capitalizing on its 24/7 availability, capital efficiency (offering ~4% margin requirement) and transparent market price discovery. Numbers speak for themselves and in February, HIP-3 DEXs had $1.1B in open interests, up from $860M mainly dominated by commodities. Trade volume by HIP-3 DEXs also rose 62.4% MoM to $40.3B in February. Despite declining volumes on Hyperliquid dragged by softer risk appetite, adoption metrics painted an entirely different picture. Daily active users on Hyperliquid rebounded from January lows, while transactions have hit the highest in record. Growing demand from HIP-3 DEXs through uncorrelated tradfi asset offerings have helped buoyed risk off sentiment in crypto markets and further supported the revenue growth of Hyperliquid.

DeFi

Saga around the largest lending protocol Aave continues as Marc Zeller and ACI announced their departure from Aave DAO following the departure of BGD Labs as contributors could not come to a consensus over the revenue sharing agreements and the future direction of the protocol. Despite the unresolved conflicts, markets are pricing in a 60% chance on Polymarket that Aave v4 will launch by June 30 as at the time of writing. The protocol has also surpassed $1T in loan origination volume since inception with its next phase of growth focused on RWA assets.

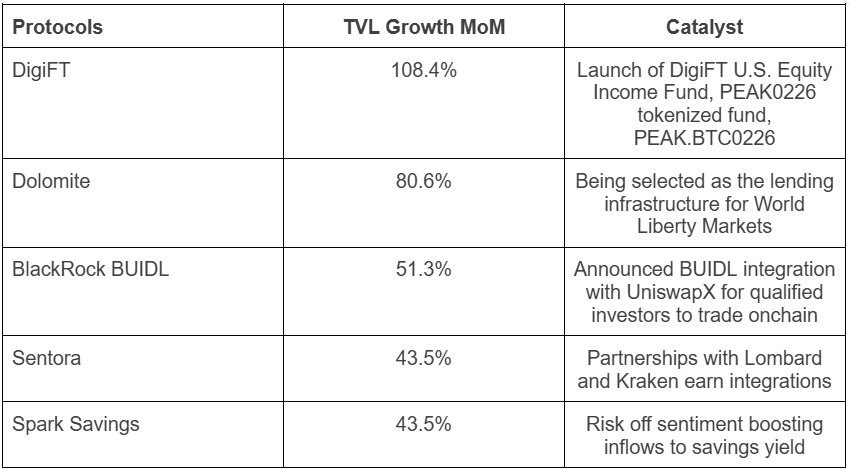

Overall, the softer sentiment in crypto is reflected in the table below although there are several protocols that saw positive performance.

New entrant, Ethereum's native ve(3,3) DEX, Supernova launched in February. It quickly rose through the ranks through incentivized yields to become the top 10 DEX on Ethereum, generating over $836M of trading volume in February.

Other notable gainers in DEX volumes:

- Balancer V3 — +95.2% ($2.05B → $4B)

- Uniswap V3 — +8.17% ($35.88B → $38.51B)

Stablecoins & Payments

Stablecoins were February's most consequential sector — not due to price action, but due to a pair of regulatory developments that will shape the market's architecture for years.

On February 26, the OCC released its 376-page proposed rulemaking to implement the GENIUS Act (passed July 2025), opening a 60-day public comment period. The proposal formally classifies payment stablecoins as non-securities under bank-style supervision, with strict 1:1 reserve requirements and a controversial yield prohibition: the OCC proposed that stablecoin issuers — and potentially third-party intermediaries — be barred from offering any yield or rewards to stablecoin holders. This directly threatens Circle's revenue-sharing arrangement with Coinbase, which generates significant income for the exchange. The industry moved quickly to push back, framing the OCC's interpretation as an overreach.

Underlying the regulatory headwinds, real world adoption of stablecoin continues to progress rapidly with institutional adoption outpacing consumer adoption.

Other notable developments:

- Transaction volume on Solana hit record highs in February, reaching $650B.

- MoonPay, M0 and PayPal launch PYUSDx, allowing stablecoins backed by $PYUSD.

- Still no notable progress in CLARITY ACT as contention surrounding stablecoin yield remains unresolved.

- SBI Holdings unveils trust bank-backed JPY stablecoin with Q2 launch target.

- Metamask Card launched in the U.S.

- Circle Q4 earnings beat estimates.

- Safe launched incentive vault for EURCV as the total value of euro-stablecoin exceeds $1.3B.

RWA

The SEC Commissioner Mark Uyeda's February 9 speech at the Asset Management Derivatives Forum emphasised that tokenisation is "no longer a theoretical exercise, but is becoming a practical reality," referencing the Commission's processing of an exemptive application under the Investment Company Act for a tokenised product. The SEC is preparing tools to position the U.S. as the "Capital of Tokenization," accelerating integration of multi-asset ETPs and atomic settlement for tokenised securities.

Onchain metrics are also showing robust growth metrics as tokenized treasuries surpassed $10B in February, while tokenized commodities and equities both notched TVL gains of 50% and ~216% MoM respectively. The catalyst for tokenized commodities was the hedge against market volatility for onchain participants while tokenized equity took a step closer to mass adoption as Ondo Finance brings its tokenized stock offerings to millions of Binance Alpha users. Tokenized equity is also seeing greater utility onchain; its use in DeFi surged from $15.3M in January to more than $330M in February as more DeFi protocols integrate them as collateral for lending and borrowing purposes.

Other notable developments:

- BlackRock's BUIDL being integrated into UniswapX for qualified investors to access 24/7 liquidity and trading.

- Ondo Finance integrates with Chainlink Data Feeds to enable tokenized securities to be used productively on Ethereum DeFi ecosystem. Euler Finance has announced the integration of Ondo's tokenized stocks to be used as collateral.

Notable Fundraising

- Japanese Yen-pegged stablecoin, JPYC, announced a $12M Series B funding led by Asteria Corporation.

- STS Digital, a digital asset trading firm, completed a $30M strategic round led by CMT Digital.

- Kraken acquired the token management platform, Magna.

- Novig, a sports prediction market platform, raised $75M in its Series B funding led by Pantera Capital.

Events in March

- Stablecoin yield negotiations: The White House's March 1 deadline for the stablecoin reward/yield compromise is the most immediate catalyst. Resolution (or failure) will directly impact Circle-Coinbase economics and set the tone for the Clarity Act's progress.

- Senate Clarity Act vote: Comprehensive U.S. crypto market structure legislation could provide structural tailwinds for regulated asset inflows if passed.

- OCC public comment period: Industry lobbying against the GENIUS Act yield prohibition may soften the framework — outcome to watch over the 60-day comment window.

- Alpenglow (Solana): Q1 2026 mainnet deployment of the sub-second finality upgrade would be a significant technical catalyst for SOL ecosystem recovery.

- 9.92M HYPE unlock on 6 March 2026

- 25.72M ZRO unlock on 20 March 2026

- 88.89M XPL unlock on 25 March 2026